Lessons Learned About EV Consumers Who Rated the U.S. Federal Tax Credit “Extremely Important” in Enabling Their Purchase

This paper, published by the 35th International Electric Vehicle Symposium (EVS35), aims to inform incentive design by increasing understanding of who was, and who was not, influenced to adopt an electric vehicle by the U.S. federal EV tax credit.

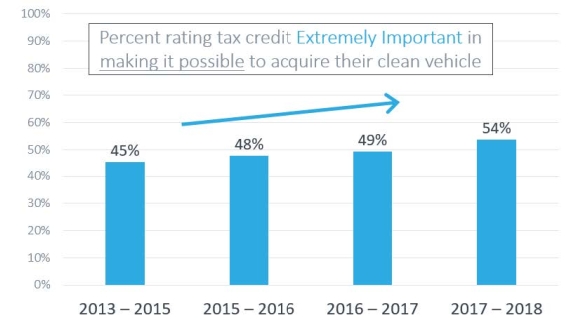

Analysis of 6,391 recipients of California’s EV rebates found that the influence of the federal EV tax credit:

- Has been increasing not decreasing—indicating it was too early to phase the incentive out.

- Increases as the purchase gets closer in time to when the consumer gets the money—indicating the incentives would be more effective if moved closer to the point of sale.

- Increases for lower-priced EVs—indicating an opportunity to limit the benefit for luxury-priced EVs and/or increase the benefit for lower-priced EVs. Both intuitive and reinforced by similar findings for state rebate programs, this provides an opportunity to increase program cost-effectiveness and equity.

- Increases with credit amount—indicating the incentive was not too big (for impactful vehicles).

- Was not related to income (for BEV consumers) or, perversely, decreased for those with lower incomes (for PHEV consumers). Unfortunately, to fully benefit from the federal tax credit, a consumer needed sufficient tax liability, meaning those with lower incomes didn’t benefit as much as those with moderate or higher incomes. The findings bore this out—indicating incentives should not depend on having tax liability.

A presentation summarizing the research is also available for download.

Read more about: